As we look back on the financial markets in 2015, what really stands out is how poor returns were across the globe and across asset classes (stocks, bonds, commodities, etc.). Among the major global stock markets, the United States was the best performer, but that’s faint praise given the S&P 500’s 1.4% return. What’s more, it was a market in which a handful of large tech/internet companies (e.g., Facebook, Amazon.com, Netflix, and Google) generated huge gains and pulled the index into positive territory. The average stock price of the index companies actually fell 2.2% for the year.

One striking feature of last year’s investment environment was the difference in the direction of the U.S. economy and U.S. monetary policy versus other major global economies. In December, the U.S. Federal Reserve (Fed) was sufficiently comfortable with the outlook for economic growth and relatively normal inflation that it raised interest rates for the first time in nearly a decade. Outside the U.S., sharply lower commodity prices (most notably oil), Middle East tensions, and China’s slower economic growth weighed on asset returns. Developed international stocks were down 0.8% and emerging-markets stocks fell 14.9%. As in 2014, the strength of the dollar was a large factor. Currency losses subtracted about 6% from developed international stock returns and about 9% from emerging markets stocks. Currency effects are always a shorter-term wild card when investing overseas, but we expect the dollar to continue to appreciate for the foreseeable future.

The worst-performing areas of the markets were commodity-related asset classes. Commodity indexes were crushed, down on the order of 25%–30% on slower growth in China and dollar strength. Oil prices hit an 11-year low in December and fell 30% for the year, after plunging 50% in 2014. Energy Master Limited Partnerships (MLPs), an increasingly popular asset class, dropped over 30%.

Fixed-income (bonds) offered little support as expectations for rising interest rates coalesced. The Barclay’s Aggregate Bond Index gained just 0.3%. High-yield bonds fared worse, down close to 5% as investors focused on default risk among some heavily indebted energy producers. Investment-grade municipal bonds were a relative bright spot, with the national muni bond index up 3.3% for the year.

Overall, 2015 was a challenging year for the financial markets in general, and for our portfolios more specifically. The major headwind to our performance was our allocation to anything other than large U.S. companies (like non-U.S. stocks). Given the challenges of the past year, it’s important to review why having positions in other assets is beneficial.

Our investment philosophy is based on the belief that fundamentals ultimately drive investment returns. This gets down to the economics of the investment. Specifically, whether we’re evaluating stocks, bonds, real estate, or another asset class, the value of an investment is ultimately determined by the cash flows the investment generates over time. That said, valuation is a very poor short-term market indicator.

Over full market cycles (five to 10-plus years), history has shown that valuation is a powerful predictor of long-term returns. Buying undervalued assets pays off over time, but it can be uncomfortable and requires discipline as we wait for markets to turn in our favor.

The U.S. equity market has had a very strong run over the past few years and by most valuation measures is a bit stretched, even after recent declines. After six years of generally rising stock prices, investors have become somewhat complacent about the potential risk. Those risks may not be imminent, but we can’t ignore them either. Foreign stock market valuations are currently more attractive, and foreign company earnings have significantly more room to grow from currently depressed levels than U.S. company earnings. Dollar strength should continue to eat away at U.S. profit margins, further supporting investing outside the U.S.

Our positions in foreign stocks are not based on a short-term view of the market, or a prediction that a drop in U.S. stocks is imminent, or even that U.S. stocks will necessarily trail non-U.S. stocks in 2016 (although it is very tempting to say they are due!). They are based on our understanding of current valuations and potential future returns.

We are confident we will be rewarded for our current allocations to international and emerging markets stocks. But it requires patience—another core element of our investment philosophy—to hold onto (and potentially add more to) these longer-term return generators during the periods when they seem only to be generating downside-risk.

On the bond side, the Fed has begun what they have described as a gradual upward climb in short-term interest rates, and our conviction in our diverse fixed-income lineup remains solid. Our investments in flexible and absolute-return-oriented income funds, short-term high yield funds and low-volatility alternatives are designed to generate higher returns and better manage their interest-rate sensitivity versus the core bond index in a rising rate environment. While core bonds may still mitigate some of the shorter-term downside risk from stocks in our portfolios, the degree to which they can do so is more limited today because of their low yields. This past year was a good example of this, with core bonds barely positive while global stocks were negative.

Finally, given our subpar outlook for U.S. stocks and bonds, we continue to find value in diversifying strategies that can generate attractive long-term returns and provide powerful portfolio diversification benefits.

We believe our portfolios are well positioned to generate solid returns over a five-year horizon. However, it is prudent to be prepared for potentially increased market volatility and downside risk (as well as positive returns) over the shorter-term. In other words, we believe the key to successful investing ahead is to maintain the healthy patience, perspective, and discipline necessary for long-term investment and financial success.

As always, we appreciate your confidence and welcome questions about your individual situation.

Download this Fourth Quarter Investment Review report as a PDF (125kb). View reports on past quarters here.

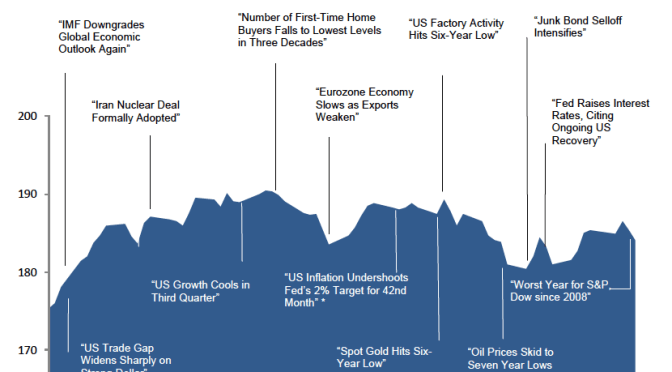

This chart shows the change in global equity markets throughout the quarter. Juxtaposed over the market performance are some of the key events that occurred during the quarter. Sometimes as we get to the end of a volatile period, it’s difficult to look back and remember everything that happened along the way.†

†Returns in US dollars. Graph Source: Dimensional Fund Advisors, Morningstar. It is not possible to invest directly in an index. Performance shown does not reflect the expenses associated with management of an actual portfolio. Past performance is not a guarantee of future results. Selected headlines are not necessarily indicative of any impact they may or may not have had on the market. *Board of Governors of the Federal Reserve System.